It happens that after buying a product or selling it, it becomes necessary to correct the written out primary. Such actions may be initiated by the supplier or the buyer if they have discovered an error in the preparation of the original delivery documents, or by ourselves, for example, when any shortages or surpluses of goods are found upon receipt of goods.

Documents created and posted in a certain period cannot in all cases be corrected or at least correctly corrected. For example, it is impossible to make changes to documents in a closed period: adjusting the receipts of previous years in 1C 8.3 may result in the reposting of many dependent documents, and as a result, a distortion of the amounts of revenue, taxes, etc. It is more correct to reflect this operation using the separate documents provided in the 1C system.

The document "Receipt Adjustment" in 1C 8.3 when purchasing goods

You can make adjustments after purchasing the necessary goods through the document of the same name in "Purchases".

And also using the "Create based on" button directly from the receipt or add it manually to the list of documents. In the case when a new document is created to change the implementation, then it must necessarily indicate the delivery document, the data of which will be corrected.

If the corrective document is entered on the basis of the delivery document, then information on the corresponding receipt will be filled in automatically and there will be no need to enter it manually. You can create the necessary documents “based on”, as an option, from the receipt document itself, or from their list.

At the same time, on the “Goods” tab, the quantity and other figures are copied from the original posted receipt document to the “Before change” line from the original posted receipt document, so this line is not available for editing. The line "After change" is automatically filled with similar values, but it is available for entering data that has been changed. You can change, reduce, or increase the quantity of goods received, as well as adjust the price if the price changes unexpectedly, for example, while the goods were moving from the supplier or the invoice operator entered erroneous data into the accounting system.

When the documents used to register the receipt are changed, there are also changes in mutual settlements with suppliers. At the same time, it is important not to forget to make changes to VAT accounting.

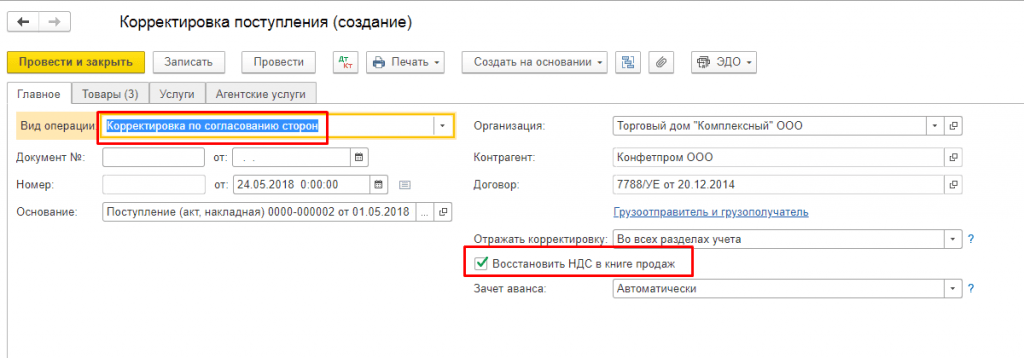

For example, when correcting a downward receipt, you must select the "Restore VAT in the sales book" flag in order to restore the VAT previously taken into account for deduction. After that, the corresponding record of the sales book is formed in the program. This becomes possible when choosing the type of the required operation “Adjustment by agreement of the parties”. In this case, in the "Goods" the VAT rate is not available for change.

You can also specify in the document whether these changes should be reflected in all relevant accounting sections or only to make changes to VAT accounting. Postings reflect the recovery of VAT and record data on the adjustment of the value of the goods.

If the operation "Correction in primary documents" is selected, corrections will be directed to errors in the primary document. Here, in order to make adjustments, all columns of the tabular part are available for change. You can also generate adjustment movements for VAT.

Based on the selected purchase adjustment documents, you can create an "Invoice Received". Data is entered using the "Create based on" button from the document itself or from the list of documents for the purchase of goods.

When the cost of purchased goods increases, it is necessary to prepare the document “Formation of purchase book entries” and fill in the “VAT deduction” tab.

The document "Adjustment of sales" in 1C 8.3 when purchasing goods

The "Create based on" button allows you to create a new document from the implementation or manually add adjustments to the list of documents.

When a new document is created, if it was generated using "Add from the list of adjustment documents", you need to make sure that it contains the sales document whose data will be corrected.

When the sale data is changed, not only mutual settlements with the buyer, but also revenue are subject to change, and accordingly - financial results firm's activities.

You need to correct the sales downwards in 1C:Accounting in the same way as adjusting receipts: select an operation (this can be either an adjustment by agreement or making the necessary corrections in primary documents) and make changes to the quantity or cost of goods sold in the corresponding columns in the context of each position of the nomenclature.

Similarly, we choose how to display the operation - in all relevant sections or in one VAT account. If you select “In all accounting sections”, the adjustment generates movements in accounting and tax accounting, as well as movements in VAT accounting registers.

If you select "Only in VAT accounting", movements are generated only according to VAT accounting registers, and the adjustment will have to be reflected manually in accounting records and accounting records. If "Only in printed form" is selected, no movements are generated.

On the basis, you can also issue a corrective invoice.

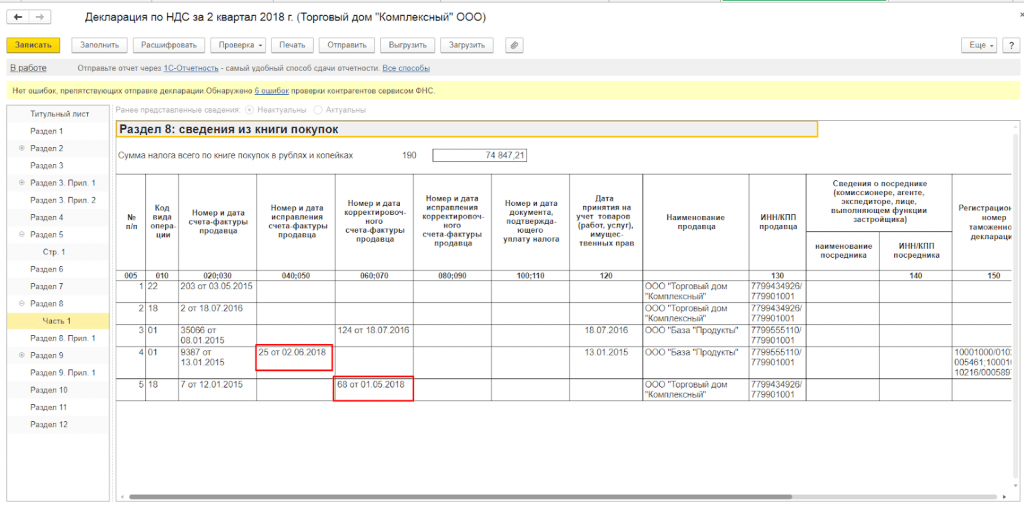

When generating purchase book entries, corrective invoices for the documents “Adjustment of receipts and sales” get there.

When generating the regulatory report “VAT Declaration”, which can be opened and generated in the “Reports” section, corrective invoices are included in the automatically completed declaration.

Thus, the 1C program has quite flexible and convenient mechanisms for reflecting various actions for the receipt and sale of products, the use of which will help to avoid accounting errors or lengthy retransmission operations.

Thus, the 1C program has quite flexible and convenient mechanisms for reflecting various actions for the receipt and sale of products, the use of which will help to avoid accounting errors or lengthy retransmission operations.

In continuation of the topic started in issue 9 (September), p. 22 "BUH.1C" for 2014, and dedicated to supporting primary accounting in "1C: Accounting 8" (rev. 3.0), we will talk about the procedure for correcting and adjusting primary accounting documents using the program, as well as how to reflect the changes made in the accounting of the seller and buyer. This article will focus on the correction and adjustment of the primary in the "paper version". The entire described sequence of actions and all the figures are made in the Taxi interface of the 1C: Accounting 8 program. In preparing the article, information was used from the Directory of Business Operations. 1C: Accounting 8" of the section "Accounting and tax accounting" of IS 1C: ITS.

The one who does nothing makes no mistakes

Even if the workflow in an organization is well-established and automated, the influence of the notorious human factor cannot be completely excluded, therefore, making mistakes when compiling documents is an inevitable reality. The representative of the seller company is not always to blame for this, since at the time of processing the primary documents and invoices, the details of the counterparty-buyer may change.

Note! The Tax Service has developed a service for checking the details of the counterparty (TIN and KPP). This will avoid errors in invoices, purchase and sales books, and invoice journals.

In "1C: Accounting 8" (rev. 3.0), the possibility of checking the TIN and KPP through the new service of the Federal Tax Service is implemented. The check is performed both when entering a new counterparty, and when changing the details of an existing one. Read more about the service on the website.

So, if an error is detected by one or another party to the transaction, then the seller must issue corrected copies of the documents, and the buyer must accept and register them. At the same time, both parties correct the accounting data if the error affected these data.

Any details of the document in which an error was made (including price, quantity and amount) may be subject to correction, while the correction does not require the agreement of the parties, and the party that discovered the error simply notifies the other party of the transaction.

As a rule, an error is allowed both in the primary document (consignment note, act) and in the invoice at the same time, although in practice there may be situations when only one of the documents needs to be corrected: either the primary document or the invoice.

If an error is made in the invoice, the seller makes a corrected copy of the invoice, which indicates the number and date of the correction. The procedure for compiling an amended invoice is approved in Appendix No. 1 to Decree of the Government of the Russian Federation of December 26, 2011 No. 1137 “On the forms and rules for filling out (maintaining) documents used in value added tax calculations” (hereinafter - Decree No. 1137).

The procedure for correcting errors in primary documents

The procedure for correcting errors in primary documents is enshrined in Part 7 of Article 9 of Federal Law No. 402-FZ of December 6, 2011 (hereinafter - Law No. 402-FZ): “Corrections are allowed in the primary accounting document, unless otherwise established by federal laws or regulatory legal acts of the authorities state regulation accounting. The correction in the primary accounting document must contain the date of the correction, as well as the signatures of the persons who drew up the document in which the correction was made, indicating their surnames and initials or other details necessary to identify these persons.. The technical side of correcting primary records is not regulated by the said Law in Article 9, therefore, in practice, various options for making corrections to primary accounting documents that do not contradict Law No. 402-FZ can be used.

According to the recommendations of the fund "NRBU" Accounting Methodological Center "", set out in the Explanation R-22 / 2013-КпТ "Introduction of corrections to primary documents" dated September 20, 2013, the most common ways to make corrections to primary accounting documents are as follows:

- making corrections in the original primary accounting document;

- issuance of a new corrective document.

Method for making corrections to the original accounting document set out in the Regulations on documents and workflow in accounting, approved. Ministry of Finance of the USSR 07/29/1983 No. 105 (hereinafter - Regulation No. 105). According to paragraphs 4.2, 4.3 of Regulation No. 105, errors in primary documents (with the exception of cash and banking) are corrected as follows: the incorrect text or amounts are crossed out and the corrected text or amounts are inscribed over the crossed out text. Strikethrough is done with one line so that you can read the corrected one. The correction of the error must be indicated by the inscription "corrected", confirmed by the signature of the persons who signed the document. The revision date must also be included. The disadvantages of this method include the following:

- when a large number changes, correction by application of Regulation No. 105 will result in the unreadability of the document;

- for electronic documents, it is impossible to make changes directly to the originally issued document due to the technical features of the design of electronic documents.

Method of issuing a new (corrective) document is based on the method of making corrections by analogy with the approved procedure for compiling corrected invoices in accordance with paragraph 7 of Appendix No. 1 to Resolution No. 1137, that is, by compiling a new corrected copy of the primary accounting document.

When applied this method it is necessary to comply with the minimum requirements of part 7 of article 9 of Law No. 402-FZ: the drawn up new document must identify the corrected document by the date the correction was made and confirm its authenticity with the signatures (with decoding) of the persons who compiled the document.

Registration by the seller of corrected documents for the buyer

The program "1C: Accounting 8" (rev. 3.0) supports the method of making corrections by issuing a new corrected version of the primary document. To ensure this methodology, the correction is reflected in the additional fields of the primary document (consignment note TORG-12, act on the provision of services): Correction No. And from. These fields indicate the number and date of the correction, similar to the correction of an invoice.

The formation of the corrected primary document and the reflection of the correction in the seller's accounting will be considered in the following example.

Example 1

On June 16, 2014, the seller Sovremennye Tekhnologii CJSC, according to the shipping documents, sold the goods to the buyer LLC Cafe Skazka in the amount of 130 pieces. for a total amount of 16,874.00 rubles. (including VAT 18%). In August 2014, the buyer discovered an error in the waybill and invoice (the quantity and price of goods were incorrectly indicated). On August 22, 2014, the seller issued and handed over to the buyer the corrected documents: waybill and invoice.

Correction by the seller of the primary document in the program is entered on the basis of the document Implementation adjustment with type of operation . The corrected invoice is reflected in a separate document. In addition, the program provides for the possibility of re-correction of primary documents and invoices.

Document Implementation adjustment Sale of goods and services where the error was found. To do this, click on the button Create based on(either from the document form or from the document list form Sale of goods and services) and select the command from the drop-down list Implementation adjustment. This creates a document of the same name. Implementation adjustment, partially filled out on the basis of document data Sale of goods and services.

Consider the further procedure for filling out the document (Fig. 1):

- in field Type of operation select an operation Correction in primary documents;

- in the fields Correction No. and from the number and date of the correction;

- in field Reflect adjustment you must select a value In all sections of the account(in this case, as a result of posting the document, postings for adjusting accounting data and movement in VAT registers will also be generated);

- in the fields of the tabular part in the row after change you must specify the corrected data for the price and quantity of goods.

Rice. 1. Correction of implementation - correction in primary documents

To print the corrected primary document, press the button Seal and select the desired print form. In our example, the command is selected Waybill (TORG-12). In the printed form of the corrected consignment note, the number and date of the original consignment note, according to which the goods were shipped, as well as the number and date of correction are indicated (Fig. 2).

Rice. 2. Corrected packing list

Implementation adjustment

STORNO Debit 90.02.1 Credit 41.01

On the cost of erroneously written off twenty units of goods;

For proceeds from the sale of twenty units of goods (only by type of accounting quantitative).

Amount NU Dt And Amount NU CT WELL).

Two entries are simultaneously entered into the sales VAT accumulation register, which reflects the accrual of VAT to the budget:

- reversing entry of an additional sheet for the amount of erroneous implementation;

- entry of an additional sheet for the amount of the corrected implementation.

To create a corrected invoice based on a document Implementation adjustment, you must press the button Issue corrected invoice.

After the document Corrected invoice issued for sale Invoice journal with sign Correction.

Features of correction of UPD

You can read about the features of using a universal transfer document (UPD) on the website.

Let's consider how to make corrections to the universal transfer document, because the procedure for correcting errors in primary documents and invoices is regulated by different regulations and varies significantly.

The complexity of making corrections to the UPD also lies in the fact that errors can be made both in indicators related to both the invoice and the primary document, and in indicators related exclusively to one of these documents.

The seller's correction of the mistakes made by issuing a new corrected invoice is fraught with negative consequences, and especially for the buyer: after all, if the corrected invoice is issued in a tax period different from the period of issuing the erroneous invoice, then the buyer will have to cancel the erroneous invoice and submit an amended declaration to the tax authority. At the same time, not every detected error entails the obligation to issue a corrected invoice.

Recall that, according to paragraph 2 of Article 169 of the Tax Code of the Russian Federation, errors in invoices (adjustment invoices) that do not prevent the tax authorities from identifying during a tax audit are not grounds for refusing to accept tax deductions:

- seller;

- buyer of goods (works, services), property rights;

- name of goods (works, services), property rights;

- their cost;

- tax rate;

- the amount of tax charged to the buyer.

Based on this rule, it can be concluded that errors in invoices that do not prevent the right to deduct VAT (we will call them “non-preventing errors”) are, for example, errors in the details of the consignor and consignee, in information about the payment and settlement document, in information about the country of origin of the goods and the number of the customs declaration.

If such “non-obstructive errors” are found, new copies of invoices are not drawn up (clause 7 of Section II of Appendix 1 of Resolution No. 1137).

A separate Appendix No. 7 to the letter of the Federal Tax Service of Russia dated October 17, 2014 No. ММВ-20-15 / 86@ “On Correcting the Universal Transfer Document” is devoted to making corrections to the UPD in connection with the detection of errors.

According to the explanations of the tax department, the procedure for correcting detected errors in the UPD depends on the assigned status of the UPD and on the qualification of the error.

Recall that the status of the UPD is a service attribute that is informational in nature and which can take on the value "1" or "2". If the value "1" is indicated in the Status field, then the document is used simultaneously as an invoice and primary accounting document, if the status value is "2", then the UPD will be used only as a primary accounting document.

- corrections are made to the UPD with the status "1";

- errors were made in indicators related simultaneously to both the primary document and the invoice;

- however, errors in the part of the invoice are qualified as "obstructive errors".

In all other cases, the new UPD should be drawn up with the status "2".

If errors are made in indicators related only to the primary document, then you can draw up a new UPD with status "2" or correct the information directly in the UPD by applying Regulation No. 105 (strikethrough and correction).

In the case when it is necessary to correct the fact of erroneous recognition of the operation:

- exempt from taxation in accordance with Article 149 of the Tax Code of the Russian Federation;

- erroneous determination of the place of sale of goods (works, services, property rights) in accordance with Articles 147, 148 of the Tax Code of the Russian Federation

to change the data on the cost of shipment, you can create a new UTD with the status "2" or correct the information directly in the UTD. In this case, a separate invoice must be issued.

If, under the terms of Example 1, the seller uses UPD in his workflow, then, guided by the recommendations of the Federal Tax Service, the error in the quantity and price of the goods is corrected by compiling a new UPD with the status "1". In "1C: Accounting 8" this option is provided automatically if after saving the document Implementation adjustment by button Seal call command Universal transfer document (UPD).

Example 2

On July 24, 2014, the seller Sovremennye Tekhnologii CJSC sold goods to the buyer LLC Cafe Skazka for the total amount of RUB 35,400.00. (including VAT 18%). In October 2014, the seller discovered an error in the sales document and in the issued UPD - the contract number was incorrectly indicated. On October 22, 2014, the seller issued and handed over to the buyer the corrected UPD.

To correct an error in mutual settlements with the buyer, made due to the indication of an incorrect contract in the sales document, you can use the document Debt Adjustment.

To correct the primary document, including the one drawn up in the form of UPD, it is necessary to use the document Implementation adjustment with type of operation Correction in primary documents. Since the contract number is not an indicator related to the details of the invoice, the UPD must be issued with the status "2".

If, when filling out a document Implementation adjustment in field Reflect adjustment select value Only in printed form(Fig. 3), then as a result of posting the document, no postings will be generated to adjust the accounting data and movement through the VAT registers, and in the printed form of the UPD, the status "2" will be generated automatically.

Rice. 3. Correction of implementation - correction in printed form

You can correct the contract number manually directly in the printed form using the editing mode (Fig. 4).

Rice. 4. UPD - correction in the printed form of the document

IS 1C:ITS For more information about the application of the UTD and the procedure for making corrections to the UTD, see the reference book "Universal Transfer Document (UTD)"

There are no mistakes: the terms of the deal just changed

In the course of their business activities, economic entities may revise and change the terms of transactions already completed, as a result of which the cost of previously shipped goods (work performed, services rendered, property rights transferred) specified in the contract is adjusted. The cost may change as a result of changes in:

- prices of shipped goods, work performed, services rendered (for example, when providing retro discounts);

- the quantity of shipped valuables (for example, if the actual volume of delivered goods does not correspond to the original one, which is indicated in the shipping documents); at the same time the price and quantity of shipped goods, work performed, services rendered.

In contrast to the situation with a detected error, the cost adjustment is carried out by agreement of the parties. In this case, an additional agreement is drawn up to the contract (if the possibility of adjusting the conditions is not agreed in advance in the contract), a notice of a change in value, a protocol for agreeing on a price or another similar document registering a new fact of economic life, but the primary accounting documents (waybills or acts) for shipped goods (works, services, rights) do not change.

The seller issues an adjustment invoice, which is a separate document. For the adjustment invoice, the form approved in Appendix No. 2 to the Decree of the Government of the Russian Federation of December 26, 2011 No. 1137 is established.

Registration by the seller of corrective documents for the buyer

Reflection of the implementation adjustment in the seller's accounting and the possibility of generating a new primary document in the program and consider the following example.Example 3

On December 13, 2014, the seller CJSC Sovremennye Tekhnologii provided the buyer with consulting services on the use of software for the total amount of RUB 70,000.00. (including VAT 18%). Due to the fact that the buyer fulfilled the software procurement plan, he was given a discount on consulting services in the amount of 5,000 rubles. (including 18% VAT), which was signed on December 21, 2014 to change the price. On the same day, the seller issued and handed over to the buyer an adjustment invoice.

Issuing by the seller of a correction document in the program is entered on the basis of the document Implementation adjustment with type of operation . The corrective invoice is reflected in a separate document. In addition, the program provides for the possibility of re-adjusting primary documents and invoices.

Document Implementation adjustment can be entered on the basis of the document Sale of goods and services, which is subject to change, then the tabular part of the document will be filled with data on the content and cost of services before adjustment.

- in the Transaction type field, select the value Adjustment by agreement of the parties;

- in the Number and from fields, the number and date of the adjustment are indicated;

- in the Reflect adjustment field, select the value In all accounting sections;

- in the fields of the tabular part in the line after the change, you must specify the adjusted data on the price of the services provided.

Rice. 5. Correction of implementation as agreed by the parties

Rice. 6. Agreement to change the value

To generate a separate primary document that fixes the new cost of services rendered, you can use the Price Change Agreement printable form, which the program offers as part of the commands called by the Print button. The printed form of the agreement indicates the number and date of the adjustment, as well as the number and date of the original certificate of service (Fig. 6).

As a result of the document Implementation adjustment the following accounting entries are generated:

STORNO Debit 62.01 Credit 90.01.1

By the amount of the reduction in the cost of implementation;

STORNO Debit 90.03 Credit 19.09

In the amount of VAT to reduce the cost of sales.

For purposes tax accounting for corporate income tax, the corresponding amounts are also recorded in the resources Amount NU Dt And Amount NU CT for those accounts where tax accounting is supported (accounts with WELL).

To the accumulation register VAT submitted, reflecting information on the amounts of VAT presented by suppliers and contractors, a record is entered with the type of movement Coming and event VAT deductible by the reduction in the cost of sale.

To create an adjustment invoice based on a document Implementation adjustment, you must press the button Issue a corrective invoice.

After the document an entry will be made in the register Invoice journal with sign Adjustment.

IS 1C:ITS For step-by-step instructions on how to draw up a corrected and corrective invoice by the seller and how it is reflected in the purchase book and sales book, see the guide in the section "Accounting and tax accounting" - "Correction and adjustment of sales".

The seller can enter a document Implementation adjustment also based on documents: Act on the provision of production services, Report of the commission agent (principal) on sales, Implementation adjustment.

To register corrections in documents received by the buyer from the seller, it is necessary to use the document Receipt adjustment(with types of operations Correction in primary documents or Adjustment by agreement of the parties). Document Receipt adjustment can be entered on the basis of the following documents:

- Receipt of goods and services;

- Receipt of additional expenses;

- Receipt adjustment.

IS 1C:ITS For step-by-step instructions on how to register a corrected and corrected invoice by the buyer and how it is reflected in the purchase book and sales book, see the "Value Added Tax Accounting" reference book in the "Accounting and Tax Accounting" - "Correction and Adjustment of Income" section.

Universal corrective document

Details about legal framework application of the universal corrective document (UCD), about the features of its filling, as well as the formation of the UKD in "1C: Accounting 8" (rev. 3.0) we wrote in issue No. 12 (December), p. 5 "BUH.1C" for 2014.

Consider the example of the formation of a universal corrective document in the program.

Example

Let's change the conditions of Example 3. According to the agreement concluded with the buyer, the seller CJSC "Modern Technologies" sells the software and provides consulting services on the use of the specified software. The contract provides for a discount on consulting services if the buyer fulfills the procurement plan. On December 13, 2014, the seller provided the buyer with consulting services on the use of software for the total amount of RUB 70,000.00. (including VAT 18%) and issued a UPD. Due to the fact that the software purchase plan was completed by the buyer on December 21, he was given a discount for consulting services in the amount of 5,000 rubles. (including 18% VAT) and issued the UKD on the same date.

The printed form of the UKD is called by the button Seal from document form Adjustment of implementation (Adjustment by agreement of the parties) or from a document form Correction invoice issued.

The UKD will be automatically generated with the status "1", since the document is simultaneously used both as a primary accounting document (price change notification) and as an adjustment invoice.

Since the possibility of providing a discount to the buyer was stipulated in the contract in advance, and additional consent of the buyer is not required, then in the printed form of the UKD in the editing mode, you need to rearrange the position and decoding the signature of the head from the line - I propose to change the cost in the line - Notify me of price changes. In addition, you can enter Additional information for this transaction in the line - Other information(Fig. 7).

Rice. 7. UKD (price change notification)

IS 1C:ITS For more information on the application of the UKD, see the reference book "Universal Adjustment Document (UKD)" in the "Accounting and Tax Accounting" section.

Often there are situations when, after some time, errors are found in previously entered documents. In such cases, it is necessary to correct the document.

Many come back to the document, correct it and repost it. This way of correcting your own mistakes can lead to serious mistakes and consequences. In addition, it is often necessary to simply fix the data discrepancy for further proceedings with the supplier.

It is correct to make such changes using the 1C documents “Receipt Adjustment” and “Implementation Adjustment”. Consider step by step instructions how to work with them in 1C 8.3

An example of registering a downward adjustment of receipts

For example, let's take the document "Receipt (acts, invoices)". Correction of implementation in 1C 8.3 is absolutely similar to receipt. Let's say that two months ago we issued a document where we receive a certain product in the amount of 8,997.76 rubles.

After the arrival, we begin to sell the goods.

After some time, we found an error in the receipt document. The price should be different, for example, 223 rubles. The amount, respectively, is 9,143 rubles.

There are discrepancies:

- in mutual settlements;

- in VAT accounting.

To fix and correct this situation, there is a document "Receipt Adjustment".

Correction can be of two types:

Get 267 1C video lessons for free:

- Correction in original documents.

- Adjustment by agreement of the parties.

The differences are that in the first case we simply correct our mistake found in the original document. In this case, all columns of the tabular part are available for editing. Can .

When adjusting by agreement of the parties, that is, when the parties have agreed that the terms of delivery change (the price or quantity changes), the column with the VAT rate cannot be edited. But you can check the "" box and also create a corrected invoice in 1C 8.3.

Example of income adjustment for past period downward:

In addition, it is possible to choose where the adjustment will be reflected:

- in all sections of accounting;

- only in VAT accounting;

- only in printed form (when correcting the primary document).

Let's see the postings that the adjustment document created in 1C:

As you can see, the document corrects the difference in account 60.01 and VAT (account 19.03). In this case, if after the change the amount decreases, the VAT is reversed, and the 60th account is posted as a debit.

Adjustment- this is a change in the initial price of a product or service that occurred after shipment by mutual agreement of the parties (buyer and supplier).

If the cost of already shipped goods (works, services rendered) changes, then the seller of goods (works, services) is obliged to issue a corrective invoice. This can happen with a decrease (increase) in the cost and quantity (volume) of goods (works, services).

In the adjustment invoice - the invoice indicates the new cost of goods (works, services), as well as the change in cost. Before you put it up, you must obtain the consent of the buyer for the adjustment.

If the seller has issued an adjustment invoice to reduce the cost of goods, then the buyer makes postings according to, earlier. To do this, write back:

- Dt 68 - Kt 19;

- Dt 19 - Kt 60.

In addition, the buyer must adjust the cost of the goods themselves, attributing the difference to the account 90-2.

The seller, in turn, must make a downward adjustment to the amount of accrued VAT. For this, a reverse is done:

- - Kt 90 / "Revenue" - by the amount of reduction in the cost of goods;

- Dt 90 / “VAT” - Kt 68 / “Calculations for VAT” - for the amount of VAT from the difference.

Let's look at an example.

During May 2013 Firm "A" (seller) sold to Firm "B" (buyer) goods worth 118,000 rubles. (including VAT - 18,000 rubles). The cost of goods amounted to 86,000 rubles. Also, subject to timely payment (before the 10th), the buyer is given a discount of 5%.

Company A will make the following entries:

| date | Account Dt | Account Kt | Sum | Contents of operation | Document |

| .2013 | 62 | 90 | 118000 | Receipt of proceeds from the sale of goods | Payment order |

| .2013 | 90 | 68 | 18000 | Calculation of VAT from the received proceeds | Payment order |

| .2013 | 90 | 41 | 86000 | The cost of goods is included in current expenses | Payment order |

| .2013 | 62 | 90 | 5900 | Revenue adjustment for the amount of the increased cost of goods | |

| .2013 | 68 | 90 | 900 (5900*18/118) | Delivered for VAT deduction | Correction invoice |

Receipt Adjustment: Postings in the Past

On 12/12/2014 Firm "A" accepted work on the construction of the facility from Firm "B". They were paid in the amount of 1,200,000 rubles. (including VAT - 200,000 rubles). In May 2015, according to the results of the audit, it was established that the work was not completed in full, although they were paid. The amount of the overpayment amounted to 470,000 rubles. (including VAT - 000 rubles).

As a result, Firm "A" sent a claim and an additional agreement to reduce the cost of work to Firm "B". In May 2015, Firm B signed an additional agreement, and the overpayment was refunded.

Company A made the following entries:

| date | Account Dt | Account Kt | Sum | Contents of operation | Document |

| 12.12.2014 | 20 | 60 | 1000000 | Reflection of costs for work performed by the contractor | Payment order |

| 12.12.2014 | 19 | 60 | 200000 | Reflection of the presented VAT | Payment order |

| 12.12.2014 | 68 | 19 | 200000 | Accepted for VAT deduction | Payment order |

| 12.12.2014 | 60 | 1200000 | Payment for work performed | Payment order |

| date | Account Dt | Account Kt | Sum | Contents of operation | Document |

| .2015 | 76.2 | 91.1 | 400000 | Reflection of other income | Additional agreement |

| .2015 | 76.2 | 68 | 70000 | VAT recovery | Additional agreement |

| .2015 | 76.2 | 470000 | Funds received | Claim |

Firm "B" makes the postings:

| date | Account Dt | Account Kt | Sum | Contents of operation | Document |

1C experts tell how the user can correct his own mistakes of past years, made in accounting and tax accounting for income tax.

To simplify accounting for income tax in the program "1C: Accounting 8" edition 3.0, the following mechanism is implemented to correct errors of previous years related to the reflection of the receipt of goods (works, services). If errors (distortions):

- led to an underestimation of the amount of tax payable, then changes in tax accounting data are made for the previous tax period;

- did not lead to an underestimation of the amount of tax payable, then changes in tax accounting data are made in the current tax period.

If the taxpayer still wants to exercise his right and submit to the tax authority an updated income tax return for the previous period (in the case when errors (distortions) did not lead to an underestimation of the tax amount), then the user will have to adjust the tax accounting data manually.

Example 1

To correct errors in overstating the costs of the previous tax period, a document is also used. Receipt adjustment with type of operation Correction in original documents. The difference is that the date of the founding document and the date of the adjustment document refer to different years: in field from document Receipt adjustment indicate the date: 29.02.2016 . After that, the document form Receipt adjustment on the bookmark Main modified: in the details area Reflection of income and expenses field appears instead of radio buttons Item of other income and expenses:. In this field, you need to specify the desired article - Profit (loss of previous years) by selecting it from the directory Other income and expenses.

The order of filling in the tabular part Services and registration of the corrected version of the document Invoice received does not differ from the order described in Example 1 in the article "Correction of the error of the reporting year in 1C: Accounting 8".

Pay attention, if the accounting system for the LLC Novy Interior organization sets the date for the prohibition of changing the data of the “closed” period (i.e., the period for which reports are submitted to the regulatory authorities - for example, 12/31/2015), when you try to post the document, a message will be displayed on the screen about the impossibility of changing data in the prohibited period. This is because the document Receipt adjustment in the described situation, makes changes to the tax accounting data (on income tax) for the last tax period (for September 2015). To post a document Receipt adjustment the date of the prohibition of data changes will have to be temporarily removed.

After the document Receipt adjustment accounting entries and records will be generated in special resources for the purposes of tax accounting for income tax (Fig. 1).

Rice. 1. The result of posting the document "Receipt Adjustment"

In addition to entries in the accounting register, corrective entries are entered in the accumulation registers VAT submitted And Purchase VAT. All entries related to the VAT adjustment for the third quarter do not differ from the entries in Example 1 in the article "Correction of the error of the reporting year in 1C: Accounting 8", as in terms of VAT in this example the order of correction is the same. Let us consider in more detail how mistakes of previous years are corrected in accounting and tax accounting for income tax.

According to paragraph 14 of PBU 22/2010, the profit resulting from the reduction in the overvalued cost of rent in the amount of 30,000 rubles is reflected in accounting as part of other income of the current period (corrected by an entry in the credit of account 91.01 "Other income" in February 2016).

In tax accounting, in accordance with paragraph 1 of Article 54 of the Tax Code of the Russian Federation, an overestimated rental price should increase the tax base for the period in which the specified error (distortion) was committed. Therefore, the amount of 30,000 rubles. is reflected in income from sales and forms the financial result with entries dated September 2015.

To account for the result of adjusting settlements with counterparties (if such an adjustment is performed after the end of the reporting period), the program uses account 76.K “Adjustment of settlements of the previous period”. Account 76.K reflects the debt on settlements with counterparties, starting from the date of the transaction that is subject to adjustment, to the date of the corrective transaction (in our example, from September 2015 to February 2016).

Please note that the entry Amount NU DT 76.K Amount NU KT 90.01.1- this is a conditional posting, which serves only to adjust the tax base upwards and correctly calculate income tax.

In our example, the tax base increased not due to an increase in sales revenue, but due to a decrease in indirect costs. Income and expenses in the revised declaration must be reflected correctly, so the user can choose one of the following options:

Manually adjust the indicators in Appendix No. 1 and Appendix No. 2 to Sheet 02 of the revised income statement for 9 months and for 2015 (reduce sales revenues and at the same time reduce indirect costs by 30,000 rubles);

manually adjust the correspondence of accounts for tax accounting purposes as shown in Figure 2.

Rice. 2. Wiring adjustment

Since, after the changes made, the financial result for 2015 in tax accounting has changed, in December 2015 it is necessary to re-perform the scheduled operation balance reformation, included in the processing Closing of the month.

Now, when reporting is automatically completed, the adjusted tax accounting data will be included both in the revised income declaration for 9 months of 2015 and in the revised corporate income tax declaration for 2015.

At the same time, the user inevitably has questions that are directly related to accounting:

- how to adjust the balance of settlements with the budget for income tax, which will change after the additional payment of the tax amount?

- why, after adjusting the previous period, the key ratio BU = NU + PR + VR is not fulfilled?

For additional accrual of income tax from an increase in the tax base, which occurred as a result of corrections made to tax accounting, in the period of detection of an error (in February 2016), you need to enter an accounting entry into the program using Operations entered manually:

Debit 99.01.1 Credit 68.04.1 with the second subconto Federal budget

For the amount of additional payments to the Federal budget;

Debit 99.01.1 Credit 68.04.1 with the second subconto Regional budget

For the amount of additional payments to the budget of the constituent entities of the Russian Federation.

As for the equality BU = NU + PR + BP, indeed, after adjusting the previous period, it is not fulfilled. Report Analysis of the state of tax accounting for income tax(chapter Reports) for 2015 will also illustrate that the rule Accounting valuation = Tax valuation + Permanent and temporary differences not performed for partitions Tax And Income. This situation arises due to discrepancies in the legislation on accounting and tax accounting and in this case is not a mistake.

According to paragraph 1 of Article 81 of the Tax Code of the Russian Federation, the correction of an error that led to an understatement of the tax base must be reflected in the period of reflection of the original transaction, and in accounting, the correction of an error of previous years is made in the current period. Permanent and temporary differences are concepts related to accounting (“Accounting Regulations “Accounting for Corporate Profit Tax Calculations” RAS 18/02”, approved by Order of the Ministry of Finance of Russia dated November 19, 2002 No. 114n). There are no grounds for recognizing differences in the previous period, before making a corrective entry in accounting.

After the correction of an error in the period of discovery is reflected in the accounting records, the financial result for 2016, calculated according to the accounting and tax accounting data, will differ by the amount of the correction of the error - in accounting, the profit will be greater. Therefore, as a result of the document Receipt adjustment a constant difference is formed by the amount of the corrected error (see Fig. 1). After performing a scheduled operation Income tax calculation in February 2016, a permanent tax asset (PTA) will be recognized.